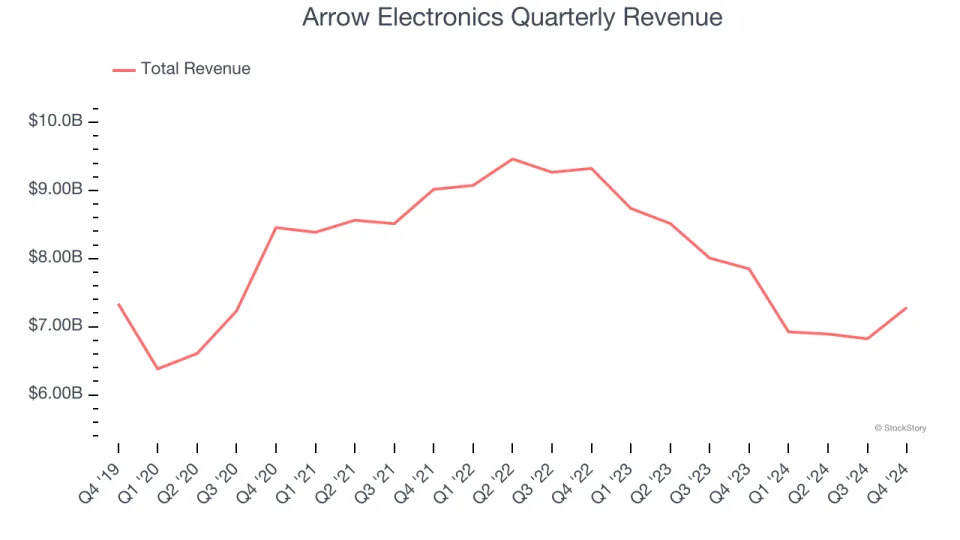

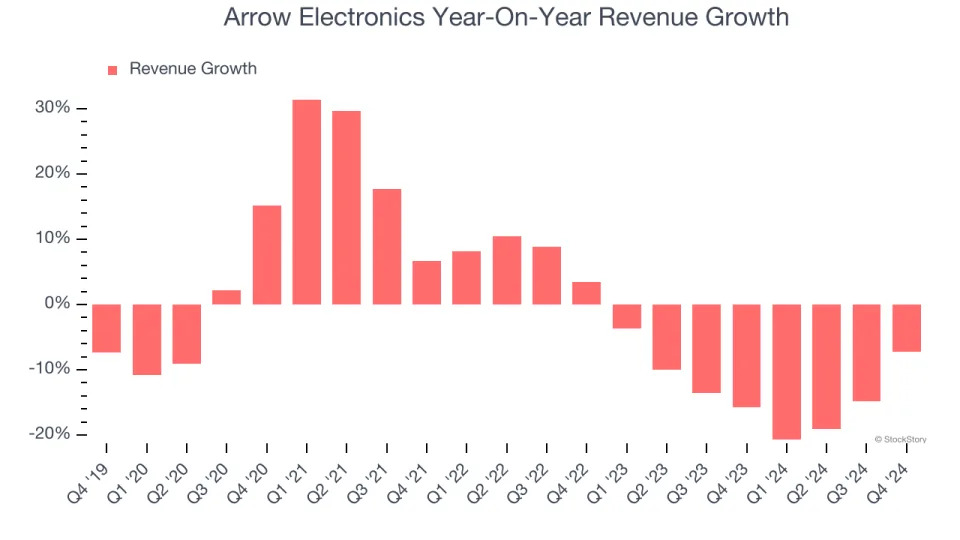

Global electronics components and solutions distributor Arrow Electronics (NYSE:ARW) reported Q4 CY2024 results exceeding the market’s revenue expectations , but sales fell by 7.2% year on year to $7.28 billion. On the other hand, next quarter’s revenue guidance of $6.28 billion was less impressive, coming in 3.3% below analysts’ estimates. Its non-GAAP profit of $2.97 per share was 11% above analysts’ consensus estimates.

Is now the time to buy Arrow Electronics? Find out in our full research report .

Arrow Electronics (ARW) Q4 CY2024 Highlights:

Company Overview

Founded as a single retail store, Arrow Electronics (NYSE:ARW) provides electronic components and enterprise computing solutions to businesses globally.

Engineered Components and Systems

Engineered components and systems companies possess technical know-how in sometimes narrow areas such as metal forming or intelligent robotics. Lately, automation and connected equipment collecting analyzable data have been trending, creating new demand. On the other hand, like the broader industrials sector, engineered components and systems companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

A company’s long-term sales performance signals its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Arrow Electronics struggled to consistently increase demand as its $27.92 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and signals it’s a low quality business.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Arrow Electronics’s recent history shows its demand has stayed suppressed as its revenue has declined by 13.3% annually over the last two years.

Arrow Electronics also breaks out the revenue for its most important segments, Components and ECS, which are 66.1% and 33.9% of revenue. Over the last two years, Arrow Electronics’s Components revenue (electronic component sales) averaged 16.4% year-on-year declines while its ECS revenue (computing solutions and services) averaged 2.2% declines.

This quarter, Arrow Electronics’s revenue fell by 7.2% year on year to $7.28 billion but beat Wall Street’s estimates by 3.2%. Company management is currently guiding for a 9.3% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 1% over the next 12 months. Although this projection indicates its newer products and services will spur better top-line performance, it is still below the sector average.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. .

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

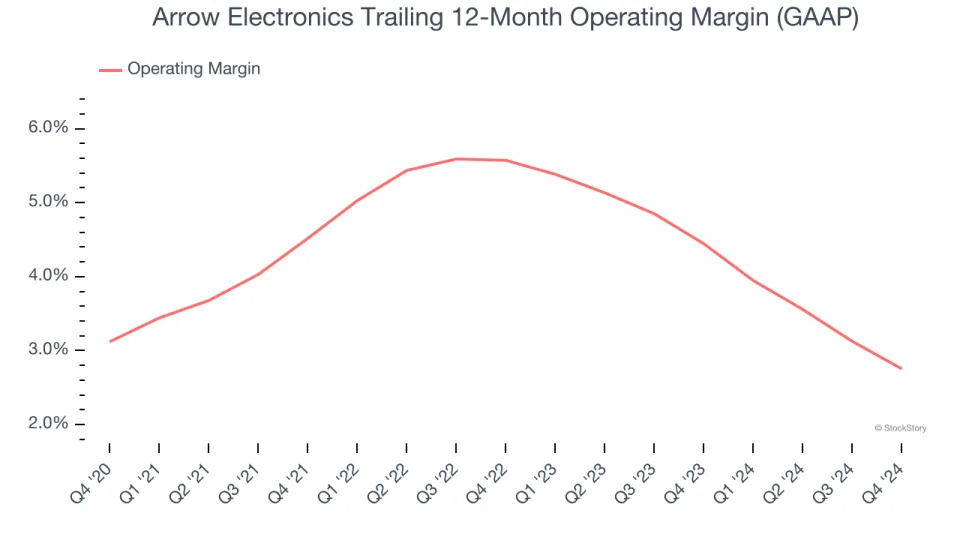

Arrow Electronics was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.2% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, Arrow Electronics’s operating margin might have seen some fluctuations but has generally stayed the same over the last five years, which doesn’t help its cause.

This quarter, Arrow Electronics generated an operating profit margin of 2.7%, down 1.4 percentage points year on year. Since Arrow Electronics’s gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, R&D, and administrative overhead expenses.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

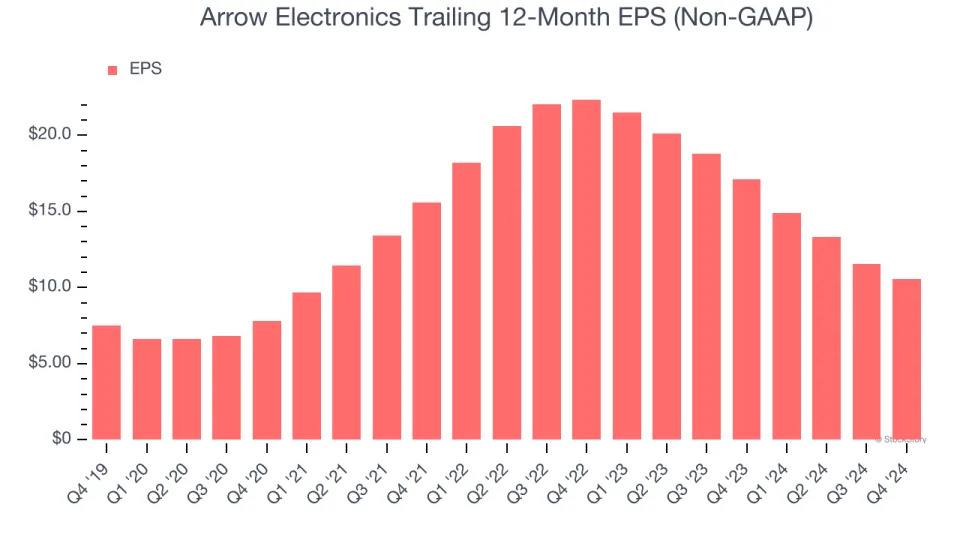

Arrow Electronics’s EPS grew at an unimpressive 7% compounded annual growth rate over the last five years. This performance was better than its flat revenue but doesn’t tell us much about its business quality because its operating margin didn’t expand.

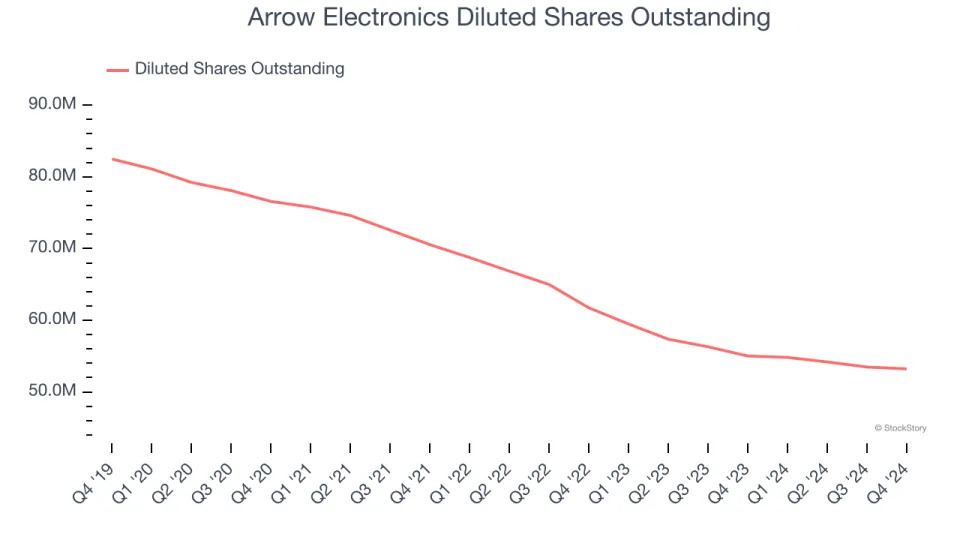

We can take a deeper look into Arrow Electronics’s earnings to better understand the drivers of its performance. A five-year view shows that Arrow Electronics has repurchased its stock, shrinking its share count by 35.5%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Arrow Electronics, its two-year annual EPS declines of 31.3% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Arrow Electronics reported EPS at $2.97, down from $3.98 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Arrow Electronics’s full-year EPS of $10.54 to grow 16.1%.

Key Takeaways from Arrow Electronics’s Q4 Results

We enjoyed seeing Arrow Electronics exceed analysts’ revenue expectations this quarter, driven by outperformance in its ECS segment. On the other hand, its EBITDA missed significantly and its revenue and EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 7.8% to $105.99 immediately after reporting.

Arrow Electronics’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free .